Tax and Customs Administration making fewer tax adjustments for false self-employment

False self-employment at low risk of detection

The Tax and Customs Administration’s approach to false self-employment in the engagement of specialists in various business sectors is meeting with little success. A law to strengthen enforcement at contracting authorities was introduced in 2016. In the face of popular opposition to the new rules, however, the government introduced an enforcement moratorium in the same year. As a result, tax officers are making fewer and fewer checks of whether contracting authorities are remitting salaries taxes and national insurance contributions when they should. The number of tax adjustments is low and the self-employed are also being checked less often.

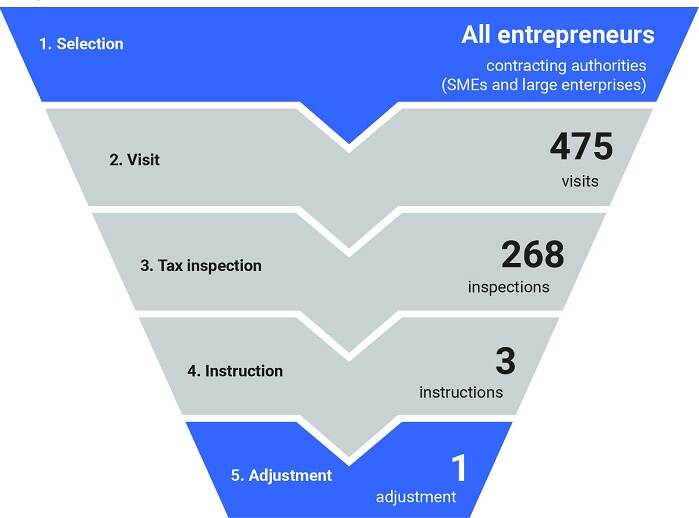

The moratorium for contracting authorities has been lifted slightly in recent years. The Tax and Customs Administration can now give contracting authorities instructions to rectify a person’s employment status if it suspects false self-employment. In a focus investigation published on 5 April 2022, however, the Netherlands Court of Audit reports that the Administration gave only 3 instructions and made only 1 tax adjustment between the end of 2019 and 2021.

The Court of Audit analysed the data in 1.1 million tax returns to see how often the Administration had adjusted the tax returns of the self-employed. The number has been declining since 2016. With its current resources, the Administration is unlikely to detect false self-employment in advance or in hindsight.

Employment status instructions and tax adjustments

Little interest in tools

The Court of Audit also found that enterprises asked the Administration for advance assurance on whether an arrangement to engage self-employed persons was correct less often. Enterprises and other organisations engage the self-employed partly because they are less expensive than employees owing to the lower tax remittances. The Administration has developed tools to clarify labour relations in recent years, including a web-based module to make it easier for contracting authorities and the self-employed to observe the law, but little use is made of the tools. In the current coalition agreement, the document setting out the government’s ambitions, a great deal is expected of the web-based module.

For its focus investigation, the Court of Audit interviewed officers from the Tax and Customs Administration and parties active in the labour market. Like the tax officers, organisations of contracting authorities, the self-employed and trade unions are calling for rapid changes. As things stand at present, false self-employment distorts the labour market and the Administration’s weak enforcement cannot rectify the situation. Weak enforcement is also losing the government tax and contributions revenue. The longer it takes to find a solution, the greater the problem will become. Specialists at the Tax and Customs Administration are calling for a gradual lifting of the current enforcement moratorium. The two previous governments left it to the next government to find a permanent solution to the problem.

Shortage of enforcement officers

To put it bluntly, enforcing all the tax rules of the Assessment of Employment Status (Deregulation) Act (WDBA) is not a viable long-term option. It would only create opposition again among the enterprises that engage self-employed persons. Neither is it a realistic option for the Tax and Customs Administration. Distinguishing false self-employment from self-employment is a labour intensive task and under the current laws and regulations the Administration has too few specialised officers for a reintroduction of the necessary supervision work, which has now been largely suspended.

| The Netherlands counts more and more self-employed persons. There are currently 1.1 million, versus 8 million employed persons. Before 2016, 500,000 declarations of employment status had been issued to the self-employed. The declarations release employers from liability to fines and for salaries tax and national insurance remittances. They give contracting authorities assurances about a self-employed person’s employment status. However, they also encourage false self-employment. As contracting authorities run no tax risks, for financial reasons they are more inclined to engage self-employed persons, even for many hours and over longer periods of time. In cases of self-employment, the self-employed and the contracting authorities enjoy certain tax benefits, but not in cases of false self-employment. The WDBA must put an end to false self-employment by making the contracting authorities partly responsible but it has not been enforced in practice owing to the opposition from enterprises and the self-employed. |