The financial processes relating to the JSF programme

International cooperation, national audit

Are we paying the right amount for the JSF? That was the central question in this audit. To answer it, the Netherlands Court of Audit and the Office of the Auditor General of Norway asked two questions of the JSF Program Office in Washington: Is the JPO providing all international partner countries with sufficient assurances that calls for funds made by the commercial contract parties in the JSF programme are in agreement with the contract and other applicable agreements and regulations? and, Can the partner countries’ Ministries of Defence be confident that their contributions to the JSF programme are correct and consistent with agreed cost allocations and that the contributions are in keeping with all contracts, agreements and regulations governing the JSF programme?

The calls for funds the Netherlands receives from the United States for the development and procurement of the JSF fighter aircraft contain a considerable number of errors. Fortunately, they are identified and corrected promptly by the Ministry of Defence. An audit carried out by the Netherlands Court of Audit and the Office of the Auditor General of Norway has resulted in The Hague receiving more financial information via the Pentagon from the American companies concerned. Further to its investigation, the Court of Audit made a series of recommendations that are also relevant to the Netherlands’ future foreign military procurement projects.

Audit with the Office of the Auditor General of Norway

The audit report published on 31 October 2018, Financial Processes for the JSF – International cooperation, national audit, was carried out at the Pentagon partly in cooperation with the Office of the Auditor General of Norway. It is the first time that foreign supreme audit institutions (the Dutch and the Norwegian, both countries are partners in the JSF Project) have examined the financial processes surrounding the Joint Strike Fighter in the US. Not even the US Government Accountability Office has done so.

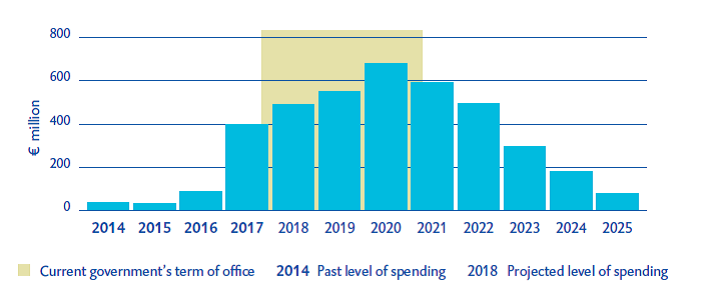

Expenditure on JSF project peaks during current government's term of office

Sharing information with international partners

In response to our audit, earlier agreements on the provision of information regarding the JSF project have been correctly implemented by the US and improved on certain points. For many years, the JSF Program Office (part of the Pentagon) did not share audit reports issued by US institutions on the accuracy of commercial invoices raised by the aircraft builders Lockheed Martin and Pratt & Whitney with the eight international partners taking part in the programme. The Dutch Minister of Defence therefore had to make additional agreements with the US aircraft builders to give audit institutions access to the information.

Errors in recharged costs

The audit in the US found errors in the JSF costs recharged to the international partner countries. The Netherlands Court of Audit then established in the Netherlands that the Minister of Defence strictly checked the payment requests. Between January 2017 and June 2018, Dutch civil servants found and corrected 59 errors in 838 payment requests.

Findings relevant to other military investment projects

The Court’s audit highlighted the need to carry out additional checks of the payment requests in the Netherlands and other partner countries. A minister in a partner country must be satisfied that the financial checks satisfy the applicable standards and agreements. They can then be included in the minister’s report to parliament on expenditures and revenues.

According to the Court of Audit, the audit findings and recommendations are also relevant to other, future projects to procure military materiel where foreign payments are often spread over many years.

What are our recommendations?

- We recommend that the Minister of Defence put appropriate procedures in place from the outset when entering into new international investment projects to ensure that costs are correctly allocated and audited.

- We further recommend that the minister always receive and check the information from the other partners that she needs for accounting purposes.

- We recommend that international agreements specifically state that the Netherlands Court of Audit must have unhindered access to the information.

- We therefore recommend that the minister check calls for funds as to the correct application of the cost allocation percentages.

- We also recommend that the Minister of Defence satisfy herself in the years ahead that the DMCA/DCAA’s checks of payment requests are reliable.

- The minister should use her powers of persuasion in the JSF programme organisation to strike a balance between the feeding and the use of the partners’ dollar deposits.

Why did we audit the payments for the JSF fighter aircraft?

To account correctly for the JSF expenditure, the Minister of Defence is highly reliant on information received from the US, which is difficult to audit. The Netherlands’ Government Audit Service (ADR) has also run into this problem. At the request of the House of Representatives it issues an auditor’s report on the JSF progress reports. As a matter of course, the ADR includes a disclaimer in its reports, stating that it cannot express an opinion on the reliability of the information received from the US.

Since 2009, the US government has been working on a programme to improve the federal government’s annual accounts. Its aim is to have all government departments publish accountable financial statements in due course. This includes the JPO, which is part of the Department of Defense. To implement the federal programme, the JPO has introduced its own action plan known as the Joint Asset Reporting and Accounting (JARA) initiative. It is designed to ensure that the JPO can render account to the federal government and the international partners. To date, however, the JPO has not published any financial statements.

The Office of the Inspector General (OIG) is comparable to the Dutch Government Audit Service. In the American system, the OIG carries out the internal financial audit of the departments but to date it has not investigated the financial processes in place for the JSF programme. The Government Accountability Office (GAO) carries out the annual audit of the JSF programme but to date it, too, has not examined the financial processes.

There has therefore been no independent US audit of the JSF programme’s financial processes that the national audit institutions in the partner countries can rely upon. This makes it difficult for these institutions to give their parliaments assurances on the regularity of the use of the JSF funds. That is why we thought it necessary to audit whether the amounts we are paying for the JSF are correct.

What standards and methods did we use in this audit?

To determine whether the amounts we are paying for the JSF are correct, we carried out an audit in cooperation with the Office of the Auditor General of Norway of the financial processes at the JPO in Washington. To do so, we exercised the audit rights in place for the programme. Further to the joint audit findings we each audited the associated financial processes and procedures in our home countries separately. We asked whether the DCMA/DCAA checks satisfied the US standards. There was reason to doubt that they did, as the GAO and the OIG had on several occasions criticised the way in which the DCMA/DCAA had carried out checks in recent years. The GAO reported in 2012 that the DCMA/DCAA was slow to audit the business systems used by the Department of Defense’s suppliers and sometimes did not audit them at all even though the suppliers had an Approved status. The OIG reported in 2015-2016 that the DCMA inadequately monitored the development of weaknesses in the suppliers’ business systems. It also made too little use of the sanctions available to it to bring about improvements at the suppliers.

Before our joint audit, the JPO shared and discussed the audit reports issued by the DCMA/DCAA only with the US partners in the JSF programme (the US Air Force, US Navy and US Marine Corps). Foreign partners were excluded. During the joint audit, we convinced the JPO that it was unfair to deny foreign partners access to the information in the DCMA/DCAA reports. Lockheed Martin and Pratt & Whitney had, after all, signed Non-Disclosure Agreements (NDAs) with the defence ministries of the eight partner countries, in which the partners undertook to treat proprietary information they received on the two aircraft manufacturers in confidence. On the basis of the NDAs, the partner countries should also have access to the information in the DCMA/DCAA reports on Lockheed Martin and Pratt & Whitney. The Norwegian and Dutch defence ministries subsequently received part of the reports; it is not known whether the other partner countries have also received this information.

The national audits are closely related to the joint audit. The joint audit investigated the procedures in the United States and the national audits expressed an opinion on the related procedures in place in the Netherlands and Norway for the JSF Project. Our key audit question was, To what extent do national audits of calls for funds from the JPO provide assurances on the regularity of the Netherlands’ expenditure on the JSF Project?

Current status

The Minister of Defence responded to the audit conclusions and recommendations on 12 October 2018. The Netherlands Court of Audit presented its response to the minister in an afterword in the report. The report was published on 31 October 2018.